Step 1

Advice on tax residence, double taxation, and income and wealth taxation.

We assess your eligibility for the NIR regime and advise on the implications for your global income and wealth.

RPBA lawyers have an in-depth knowledge and expertise in Personal Residence Planning.

The Portuguese non-habitual tax resident regime 2.0 enables a very attractive taxation for global High Net Worth individuals.

The Portuguese Golden Visa for non-EU investors grants access to the entire Schengen Area.

The Madeira Free Zone provides many interesting tax structuring opportunities.

Real Estate Tax Structuring is crucial on the acquisition of high-end rental estate by non-Portuguese residents.

This website also contains legacy information on the Non-habitual tax resident (NHR) regime has been revoked with effect from January 1, 2024, onwards, as per the Portuguese Budget Law for 2024.

If you want to know more about the IFICI+ (Incentivo Fiscal à Investigação Científica e Inovação - "Tax Incentive for Scientific Research and Innovation"), sometimes also called as Non-Habitual Resident (NHR) 2.0 or New Inpatriate Regime (NIR), please find the

link to our presentation on the NIR, which has now been fully implemented (law, ministerial orders, tax administration guidance, lists of qualifying activities, forms, IT system).

Currently, there is also a tax benefit in place for people who (i) became/become tax resident in Portugal until 2026 (ii) have been previously tax resident in Portugal and left before a certain date; (iii) have not been tax resident in Portugal during the 3 years prior to the new residence; (iv) have their Portuguese tax obligations in good standing and (v) have not applied for the NHR regime.

Other current main features are:

• The benefit corresponds to a cut in half of the tax base (not to be confused with tax rates) applicable to all employment and self-employment income earned (from foreign and Portuguese source);

• No reduced rate as the general and progressive rates apply instead;

• No need to register for it. One can apply for its benefits while filling the tax return;

• No need to perform a specific activity to be eligible.

The benefit: (a) lasts during a period of 5 years and (b) the 50% reduction of the taxable base is limited to the first € 250,000 of income from employment and self-employment income. It is still necessary to have the Portuguese tax obligations in good standing and not apply for the NHR or the NIR. A Parliamentary amendment clarified that it is still necessary to have been resident in Portugal before; on the other hand, the applicant must not have been resident in Portugal during the 5 years prior to entry into this regime.

The “ex-residents” regime may be a viable option for newcomers obtaining employment or self-employment income either abroad or in Portugal.

If you are still interested in our Residence Planning services please scroll down below.

The cherries on top of the cake are that:

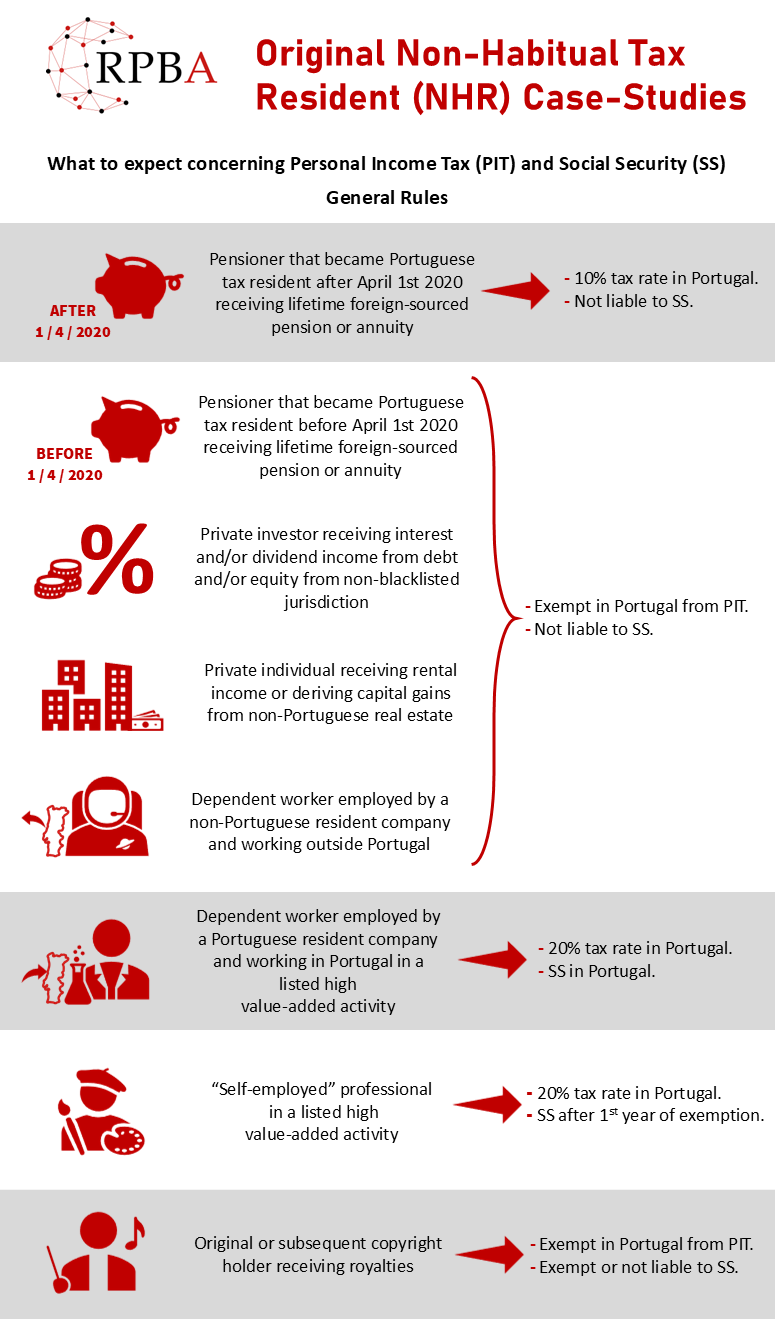

The Portuguese Non-Habitual Tax Resident regime grants an exemption on foreign source income as well as a limited taxation on income deriving from high value added activities;

The Portuguese Golden Visa regime allows non-European Union investors to access the entire Schengen Area [for more information on this please read our Newsletter (in English) and Presentation (in English)].

Since 1 January 2004 close family (spouses, children, grandchildren, parents and grandparents) is exempt from Stamp Tax on gifts and inheritances.

Moreover, the disposal of foreign assets (even towards Portuguese residents) as well as, in certain cases, the disposal of Portuguese assets towards non-Portuguese residents, are not liable to this type of taxation.Finally, Portugal has no wealth tax.

When family residence is considered, Portugal also tends to rank well, being a great place to raise children, due to safety and to both good private or public pediatric healthcare. The fact that in the destinations most favored by expats, like Lisbon, Cascais-Estoril and Algarve, English is widely spoken by the Portuguese tends to facilitate foreigners’ integration, some being able to live decades without learning the native language.

Some of the drivers of personal residence may also prove to be key factors for HNWI that are moving to Portugal to consider locating part of their dedicated Family Offices here.

Portugal has relatively cheap real estate (although tax structuring is vital as this is an overtaxed sector), namely office space, an excellent telecommunication infrastructure and educated, qualified and affordable professionals. Its location at the south of Europe, in the tip of the Mediterranean Sea and bordering the Atlantic Ocean, as well the 300 daily flights from Portugal to foreign countries make it an ideal place for globetrotters.

Its several seaports and marinas and its Exclusive Economic Zone, a sea zone of 1,727,408 km2 (the 3rd largest of the European Union and the 11th largest in the world), as well as its 31 airports and aerodromes, make it a natural choice for recreational yachting and private jet travel.

RPBA

will keep you updated with the latest awards and accolades granted to Portugal and world news about the New Inpatriate Regime (NIR), Portuguese non-habitual tax resident (NHR) and Golden Visa regimes.

Portugal is a premium destination for sun-seekers, with 3300 hours of sunshine per year, one of the highest rates in Europe.

In comparison with other major European countries, Portugal is highly affordable in particular with regard to real estate investments.

Portugal ranks among the best countries in the world for quality of life.

Portugal has a convenient location for globetrotters with approximately 300 daily flights to major world cities.

Portugal is seen as one of the most peaceful and safest countries around the globe.

One of

RPBA's expertise services is residence planning (in particular through the Portuguese IFICI+ (Incentivo Fiscal à Investigação Científica e Inovação - "Tax Incentive for Scientific Research and Innovation"), sometimes also called as Non-Habitual Resident (NHR) 2.0 or New Inpatriate Regime (NIR) or through similar foreign regimes). We frequently assist wealthy foreign individuals moving to Portugal and, likewise, Portuguese nationals moving abroad.

We also help them optimize their Portuguese real estate tax structuring and private wealth or income management by the use of holding and operational companies (namely in Portugal - in particular through the

Madeira Free Zone

-, Belgium, Luxembourg and Malta), trusts, private interest and family foundations, life insurance and wills.

If you are interested in becoming a Client please e-mail us to

communication@rpba.pt

Advice on tax residence, double taxation, and income and wealth taxation.

We assess your eligibility for the NIR regime and advise on the implications for your global income and wealth.

Obtain a Portuguese taxpayer number (NIF) - appointing a tax representative if required.

This is essential for any administrative or financial process in Portugal.

Legal assistance in the purchase or lease of real estate.

We support you through all contractual and regulatory aspects of your property acquisition or rental in Portugal.

Obtain a residence permit or registration certificate.

For non-EU nationals, we assist in obtaining a residence permit through the Portuguese Immigration and Borders Service (AIMA, formerly SEF).

For EU nationals, we facilitate registration at the local city council.

Register as a resident taxpayer.

Once residence is established, you will be registered as a Portuguese tax resident.

Request the password to access the Portuguese Tax Authority's online portal.

This step enables digital interaction with the tax authorities.

Submit an application to the NIR regime.

We prepare and file your NIR application within the applicable timeframe and ensure compliance with the eligibility criteria.

Obtain Portuguese tax residence certificates and coordinate foreign tax formalities.

We manage the issuance of tax residence certificates and assist with non-resident tax applications in your country of origin.

Activate the Electronic Post Box (Caixa Postal Electrónica).

This is the official channel for communications from Portuguese public entities.

File annual tax returns.

We provide ongoing tax compliance support, including the preparation and submission of annual tax returns.

Left to the main entry of the "Loja do Cidadão das Laranjeiras" and right to the Ismaili Center / Aga Khan Foundation; close to the Laranjeiras' subway station; there are two public parking spaces in a range of 100 meters, one underground at Rua Virgílio Correia, perpendicular to Rua Abranches Ferrão, and another in front of the Loja do Cidadão's back entry, underneath the Avenida Lusíada's viaduct. We also have parking space available in our building. Please request it in advance of any meeting.

GPS Coordinates: Latitude: N38.773625 Longitude: W9.171181

The Portuguese Non-Habitual Tax Resident (NHR) regime officially came to an end on 1 January 2024. New applications are no longer accepted, except in limited cases during 2024 for individuals who can demonstrate that they had already taken concrete steps to relocate to Portugal before that date — for instance, by signing a lease, purchasing property, or initiating a visa process. A grandfathering rule has been introduced to safeguard existing beneficiaries, allowing them to continue enjoying the regime’s benefits for the remainder of their 10-year period. Accordingly, the information provided below remains relevant for current NHR beneficiaries and for those who may still qualify under the transitional provisions established for 2024. Additionally, you can view and download here a presentation with these frequently asked questions together with reasons to move to Portugal.

![]()

![]()

![]()

![]()

![]()

I — Professional activities (PCP codes):

112 — General manager and executive manager

12 — Manager of administrative and commercial services (v.g., financial, human resources, and strategy)

13 — Production and specialized services' managers (v.g., farming, livestock, forestry, fishery, mining industry, transports and others

14 — Managers of hotel business, restaurants/catering, trade and other services

21 — Experts in physics, mathematics, engineering and similar technics (v.g., chemistry, statistics, urban planning, and others)

221 — Doctors (v.g., generalists and experts)

2261 — Dentists and stomatologists

231 — University and higher education professors

25 — IT and communication experts (v.g., software apps, web, etc.)

264 — Authors, journalists and linguists

265 — Creative artists and performing artists (v.g., musicians, cinema producers, actors, dancers, etc.)

31 — Technicians as well as science and engineering professions of intermediate level (v.g., mining industry, life sciences and others)

35 — Technicians of information and communication technologies (v.g., telecommunications and radio)

61 — Farmers and market-oriented skilled agriculture and livestock production workers

62 — Market-oriented skilled forestry, fishery and hunting workers

7 — Skilled industry, construction and crafts workers, including skilled workers of metalwork, food processing, woodwork, clothing, handicraft, printing, manufacture of precision instruments, jewelers, artisans, electricians and electronics professionals

8 — Facility and machinery operators and assembly workers, namely operators of fixed installations and machinery

Professionals' workers included in the above-mentioned professional activities shall possess at least, a level 4 of the European Qualifications Framework or Level 35 of International Standard Classification of Education, or five years of duly proven professional experience.

II — Other professional activities:

Directors and managers of companies carrying out productive investment activities may also benefit to the extent that they are engaged in the projects for which contractual tax benefits have been granted under the Investment Taxation Code (Código Fiscal do Investimento) enacted by Decree-Law nr. 162/2014, of 31 October 2014.

Please read here our November 2019 update on this matter.

Old list of Value-Added Activities of a Scientific, Artistic or Technical Nature (Ministerial Order nr. 12/2010, of 7 January)

1 - Architects, engineers and similar technicians:

101 - Architects

102 - Engineers

103 - Geologists

2 - Visual artists, actors and musicians:

201 - Theater, ballet, film, radio and television Artists

202 - Singers

203 - Sculptors

204 - Musicians

205 - Painters

3 - Auditors:

301 - Auditors

302 - Tax Consultants

4 - Doctors and dentists:

401 - Dentists

402 - Analyst Doctors

403 - Surgeons

404 - Board doctors in ships

405 - General Practitioners

406 - Dentists

407 - Dentist Doctors

408 - Physiatrists

409 - Gastroenterologists

410 - Ophthalmologists

411 - Orthopedists

412 - Otorhinolaryngologists

413 - Paediatricians

404 - Radiologists

405 - Doctors in other specialties

5 - Teachers:

501 - University professors

6 - Psychologists:

601 - Psychologists

7 - Professional services, technicians and similar:

701 - Archaeologists

702 - Biologists and experts in life sciences

703 - Computer Programmers

704 - Software consultancy and activities related to information technology and information technology

705 - Computer programming activities

706 - Computer consultancy activities

707 - Management and operation of computer equipment

708 - Activities of information services

709 - Activities of data processing, hosting information and related activities/Web portals

710 - Activities of data processing, hosting information and related activities

711 - Other information service activities

712 - Activities of news agencies

713 - Other information service activities

714 - Scientific research and development

715 - Research and development of science physical and natural

716 - Research and development in biotechnology

717 - Designers

8 - Investors, administrators and managers:

801 - Investors, administrators and managers of companies promoting productive investment, if allocated to eligible projects under tax benefits contracts awarded under the Tax Code for Investment, approved by Decree-Law nr. 249/2009, of 23 September

802 - Senior employees of companies

![]()

![]()

![]()

i. register as non-resident taxpayers;

ii. obtain residence permits (for non-EU nationals) and residence certificates (for EU nationals);

iii. register as tax residents; and

iv. only then apply for the non-habitual resident status.

![]()

![]()

![]()

![]()

![]()

A new change to the NHR regime could happen, but it is not likely, as the regime was introduced in 2009 by a government of the same center-left wing party (“Partido Socialista”) as the present government, which has parliamentary majority until October 2026. Additionally, there is currently no significant public debate or controversy surrounding the NHR regime.

In any case, if such change happens:

i. Even if NHR status is abolished, it cannot be taken away from those that already have it at the time the change is approved;

ii. Although the NHR status cannot be taken away, the regime could be made less attractive (reducing the scope of the exemptions, for instance) even for those that have obtained it in the past. To what extent such change could be made is very debatable under Portuguese administrative and constitutional law. Some changes would always be admissible, but in principle a change that would make the NHR regime purely nominal (making NHR and normal residents taxed in the same way or with only very minor differences) should not be allowed. Assessing the degree of change that is allowed is very difficult.

![]()

![]()

![]()

In November 2015, the Socialist party, with the parliamentary support of three far-left parties (the Left Block, the Communist and the Green parties) formed a new government. The Socialist party proposed in its electoral program the reintroduction of inheritance taxation between spouses and direct line descendants for “high value” estates (in principle those with a taxable value above 1 million Euros, with a rate of 28% applying to the surplus), but “taking into account the need to avoid phenomena of multiple inheritance taxation”. It was therefore possible that a mild form of inheritance taxation might be re-introduced in Portugal, but it is not clear how it would target NHR with non-Portuguese assets, due to the caveat in commas.

Currently, inheritance between direct family is tax exempt, assets outside Portugal are not taxable and when tax is due on Portuguese assets it is so at a low rate - 10%. The Government Program of 2015 intended to tax those exempt cases (most notably those of inheritances between direct family). However, the relevant aspects remained fully uncertain (for instance, if foreign assets would be taxed or not, if donations would be taxed in the same way as inheritances or not, how should the € 1.000.000 be valued, etc.).

The 2015-2019 legislature went by and the Government apparently gave up on the idea of amending inheritance taxation. The Socialist party electoral program of 2019 and 2022 and the Socialist government programs for the legislatures of 2019-2023 and 2022-2026 have no mention whatsoever to changes in inheritance taxation. Nevertheless, developments on this issue should be monitored.